Navigating the world of pension plans in Canada can be overwhelming, especially if you’re new to the subject. With numerous options and complex terminology, it’s essential to have a comprehensive guide that simplifies the process and empowers you to make informed decisions about your retirement savings. In this article, we will break down pension plans into easily digestible pieces, explain the various types of plans available, and provide valuable insights to help you secure a financially stable future. Let’s embark on this journey together and unravel the mysteries of pension plans in Canada.

Understanding Pension Plans in Canada

Pension plans play a vital role in retirement planning, providing individuals with a reliable income stream during their golden years. In Canada, two common types of pension plans are defined benefit and defined contribution plans. Before we delve into the details of these plans, let’s understand what they are and how they differ:

Defined Benefit Pension Plans

What is a Defined Benefit Pension Plan?

A defined benefit pension plan is designed to provide employees with a specific retirement benefit. The amount of this benefit is determined by a formula, which typically considers factors such as the employee’s salary history, years of service, and a multiplier. This formula ensures that employees have a clear understanding of the pension benefit they will receive upon retirement.

How Does a Defined Benefit Pension Plan Work?

In a defined benefit pension plan, the employer bears the investment risk and is responsible for ensuring that there are sufficient funds to fulfill the pension obligations. Contributions from both the employer and the employee are made to the pension fund, and the funds are invested to generate returns over time. These returns, along with the contributions, form the basis of the pension benefit. The employer is responsible for managing the investments and making sure that there are enough funds to pay out the promised benefits to the employees when they retire.

Advantages of Defined Benefit Pension Plans

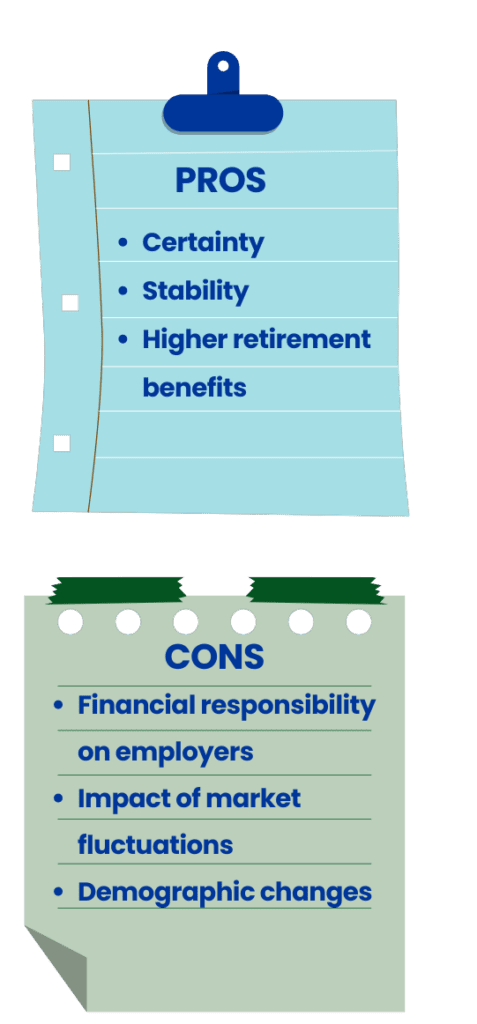

One of the significant advantages of defined-benefit pension plans is the certainty they provide. Since the retirement benefit is predetermined, employees have a clear idea of what to expect when they retire. This stability can offer peace of mind and allow individuals to plan for their future with confidence. Additionally, defined benefit plans often provide higher retirement benefits compared to other types of pension plans, making them attractive to employees seeking a reliable income stream during retirement.

Disadvantages of Defined Benefit Pension Plans

While defined-benefit pension plans offer many advantages, they also come with some potential drawbacks. One challenge is the financial responsibility placed on employers. As employers guarantee a specific retirement benefit, they must ensure that the pension plan is adequately funded to meet future obligations. Market fluctuations and changes in demographics can impact the financial health of the plan, potentially requiring additional contributions from the employer to maintain solvency.

Defined Contribution Pension Plans

What is a Defined Contribution Pension Plan?

In contrast to defined benefit plans, defined contribution pension plans focus on the contributions made by both the employer and the employee. The retirement benefit is not predetermined but depends on the contributions made and the performance of the investments over time. Employees have more control over their retirement savings and investment choices within the options provided by the plan.

How Does a Defined Contribution Pension Plan Work?

In a defined contribution pension plan, contributions are made regularly by both the employer and the employee. These contributions are invested in various options, such as stocks, bonds, or mutual funds, chosen by the employee from the options provided by the plan. The value of the retirement benefit is not predetermined but depends on the contributions made and the performance of the investments over time. At retirement, the accumulated funds are used to provide a retirement income stream for the employee.

Advantages of Defined Contribution Pension Plans

One of the key advantages of defined contribution pension plans is the flexibility they offer. Employees have control over their investment choices within the options provided by the plan. They can tailor their investments based on their risk tolerance, investment goals, and market conditions. Additionally, defined contribution plans allow portability, meaning that employees can take their accumulated funds with them if they change jobs. This flexibility and portability make defined contribution plans appealing to individuals seeking more control over their retirement savings.

Disadvantages of Defined Contribution Pension Plans

While defined contribution pension plans provide flexibility, they also shift the investment risk onto the employees. The value of the retirement benefit depends on the performance of the chosen investments, which can be subject to market volatility. If the investments underperform, it can impact the retirement savings accumulated over time. Additionally, the responsibility of managing the investments falls on the employee, requiring financial literacy and active participation in monitoring and adjusting investment choices.

Other Types of Pension Plans

In addition to defined benefit and defined contribution plans, there are other types of pension plans available in Canada. Let’s explore some of these options:

Group Registered Retirement Savings Plans (Group RRSPs)

Group RRSPs are similar to individual RRSPs but are sponsored by employers. Employees have the opportunity to contribute a portion of their income to a group plan, and employers may match a percentage of the contributions. Group RRSPs provide a tax-advantaged way to save for retirement.

Deferred Profit Sharing Plans (DPSPs)

DPSPs are employer-sponsored plans that allow employers to share their profits with employees. The contributions made by the employer are based on the company’s profitability. These plans provide employees with a retirement benefit based on the company’s success.

Registered Retirement Savings Plans (RRSPs)

RRSPs are individual retirement savings accounts that allow Canadians to save for retirement on a tax-advantaged basis. Contributions made to RRSPs are tax-deductible, and the investment growth is tax-sheltered until retirement. RRSPs offer a wide range of investment options.

Registered Pension Plans (RPPs)

Registered Pension Plans (RPPs) are pension plans sponsored by employers, similar to defined benefit and defined contribution plans. RPPs provide retirement benefits based on specific criteria set out in the plan, such as years of service and earnings. These plans offer retirement security and often include employer contributions.

Factors to Consider

- Employer Contributions: Evaluate the employer’s contribution matching policy and consider the impact on your retirement savings.

- Investment Options: Assess the available investment options within the plan and ensure they align with your investment preferences and risk tolerance.

- Fees and Expenses: Consider the fees associated with the plan, such as administrative fees or investment management fees, and how they may impact your overall returns.

- Vesting Period: Understand the vesting period, which is the length of time you need to be employed before becoming entitled to the employer’s contributions.

- Portability: Consider the portability options of the plan if you anticipate changing jobs in the future.

- Retirement Benefit: Evaluate the projected retirement benefit provided by the plan and assess if it aligns with your retirement goals and financial needs.

Seeking Professional Guidance

Understanding pension plans can be a complex endeavor. It is advisable to seek the guidance of a financial advisor who can provide personalized advice based on your individual circumstances, retirement goals, and risk tolerance. A financial advisor can help you navigate the options, assess the trade-offs, and make informed decisions that align with your retirement objectives.

Frequently Asked Questions

- Q: Is a pension plan the same as a retirement plan?

- A: No, in Canada, a pension plan is a specific type of retirement plan. While all pension plans are retirement plans, not all retirement plans are pension plans. Retirement plans in Canada encompass various options such as registered retirement savings plans (RRSPs), tax-free savings accounts (TFSAs), and other savings vehicles. Pension plans, however, refer to employer-sponsored plans that provide retirement benefits to employees based on specific formulas and criteria.

- Q: What happens to my pension if I change jobs?

- A: If you change jobs in Canada, the fate of your pension depends on the type of pension plan you have. In the case of a defined benefit pension plan, you may be eligible to receive a pension benefit based on your years of service and the plan’s formula. Alternatively, you may have the option to transfer the value of your pension to another eligible plan, such as a locked-in retirement account (LIRA) or a registered pension plan (RPP). In the case of a defined contribution pension plan, you can generally transfer the accumulated funds to a new employer’s plan or into a locked-in retirement account (LIRA) or a registered retirement savings plan (RRSP).

- Q: Can I access my pension funds before retirement?

- A: Generally, pension funds in Canada are designed to provide retirement income and are not easily accessible before retirement. However, there may be specific circumstances in which early access to pension funds is allowed, such as financial hardship or severe health issues. It is advisable to consult with the pension plan administrator or a financial advisor to understand the specific rules and options related to early access to pension funds.

- Q: Are pension plans mandatory in Canada?

- A: Pension plans are not mandatory for all employees in Canada. The availability of pension plans and their mandatory nature can vary depending on factors such as the employer’s size, industry, and provincial regulations. Some employees may have access to employer-sponsored pension plans, while others may need to rely on individual retirement savings vehicles like RRSPs or TFSAs.

- Q: What happens to my pension if my employer goes bankrupt?

- A: If your employer goes bankrupt in Canada, the fate of your pension depends on the type of pension plan you have. If you have a defined benefit pension plan and your employer becomes insolvent, there is typically a government-backed pension protection fund, such as the Pension Benefits Guarantee Fund (PBGF), that provides limited coverage for pension benefits. If your plan is a defined contribution pension plan, the accumulated funds are typically held separately from the employer’s assets and should remain intact, subject to investment performance.

Additional Resources

Financial Services Regulatory Authority of Ontario (FSRA): The regulatory body responsible for overseeing pension plans in Ontario, including the administration of the Pension Benefits Guarantee Fund (PBGF).

Pension Investment Association of Canada (PIAC): An organization representing the interests of Canadian pension plan investors, providing industry news, research, and resources related to pension investments.

Government of Canada – Retirement Planning: Official website providing information on retirement planning, pension options, and resources for Canadians

Wealth Solutions Hub:

- All You Need to Know About RRSPs: A Comprehensive Guide for Canadians

- Turning an RRSP to RRIF: A Comprehensive Guide for Canadians

Related Articles:

Mastering the RRSP: 5 Ways to Maximize Your Retirement Savings

Mastering the RRSP: 5 Ways to Maximize Your Retirement Savings

Long-term Care Options and Insurance in Canada: A Comprehensive Guide with 5 Key Resources

Long-term Care Options and Insurance in Canada: A Comprehensive Guide with 5 Key Resources

Retirement Planning and Inheritance: 12 Considerations to Securing Your Financial Future in Canada

Retirement Planning and Inheritance: 12 Considerations to Securing Your Financial Future in Canada

RRIF Account: A Comprehensive Guide to the Registered Retirement Income Fund

RRIF Account: A Comprehensive Guide to the Registered Retirement Income Fund

Demystifying Spousal RRSPs: A Comprehensive Guide

Demystifying Spousal RRSPs: A Comprehensive Guide

{kind=link}